Buy Now, Pay Later: A credit model on the rise?

![]() 12 minutes reading

12 minutes reading

Have you ever heard of a means of payment known as Buy Now, Pay Later? It’s a credit model known worldwide as a global trend and a promising bet to drive the retail industry. But what are the advantages in that credit model for consumers, retailers and especially companies providing financial services?

In this article, we gather the main information about this, which is the fastest growing payment method in the world and which promises to contribute to the Financial inclusion of many people in Latin America. Follow!

What is Buy Now, Pay Later?

“Buy now, pay later” is a credit model also known by the acronym BNPL, which means “Buy Now, Pay Later”. Despite the name referring to the idea of traditional installment payments (like the Brazilian credit card), there are some important differences in how it works that bring many advantages to consumers and retailers.

Unlike others means of payment, the use of Buy Now, Pay Later doesn’t depend on a banking account or credit card. BNPL extensively uses artificial intelligence and data-crossing to instantly run credit analysis within a purchasing customer journey in retail.

Since credit is granted or denied only for a specific transaction, there is less risk involved than in common operations. Check the following sections to better understand how Buy Now, Pay Later works and what its advantages are.

Inside the model: How Buy Now, Pay Later works

To learn more about how Buy Now Pay Later works, first we need to understand the players involved in that operation for the credit market.

Apart from the consumer and retailer, there’s also a player providing a platform, where the specific transaction will be conducted, and a financing party, which will take the risk for the operation.

The price billed for the consumer already includes a low fee for enabling Buy Now, Pay Later, which will allow the use of that means of payment. As soon as the purchase is finished, the retailer receives the full value for the product after the enablement fee is deducted, while the consumer will settle the installment throughout a period time, as in any payment in installments.

BNPL in action: Check out an operation example

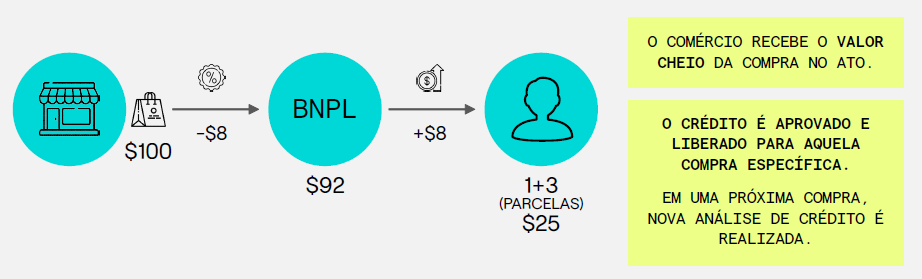

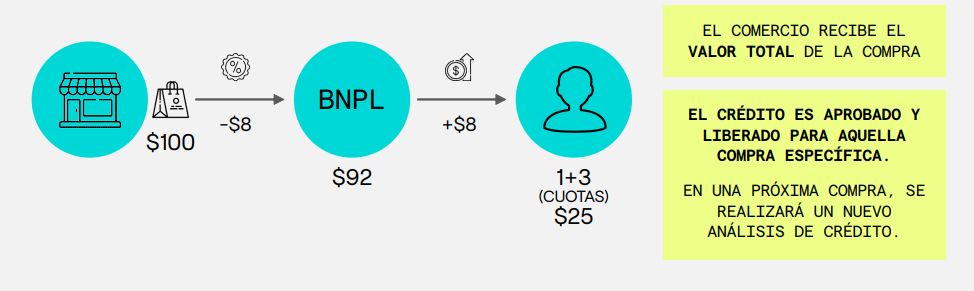

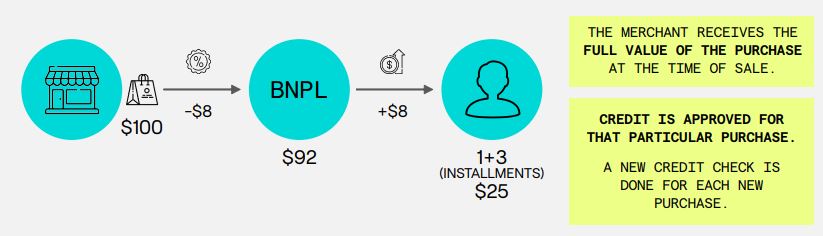

Buy Now, Pay Later is a short-term credit product that enables a consumer to make a purchase in retail and pay part of it in the future—no interest included. Take a look at an example using fictitious numbers:

- A product at a store shows the ‘actual’ price and a price that is perceived by the consumer as $100

- That specific store sells a ‘more affordable’ price (by applying a fixed value or a fee) for a BNPL player at $92, which is paid at the moment of the purchase

- The consumer pays $8 in installments, which can be paid monthly and without any interest (if the store chooses to)

- The consumer pays $100 in installments, which can be paid monthly and without any interest (if the store chooses to)

Example: 4 installments of $25 every fortnightly; the first one is at the moment of the purchase.

Since each transaction consists of a specific credit operation, the financing party, which can be a partner bank or the store’s own funding, is previously informed of the object or purpose of the purchase, which has defined dates and values.

It is, therefore, a credit solution different from models such as the card, for example, where the person granting the credit does not know in advance the purpose of using that resource, nor for how long it will last.

The improved security and transparency in that model remove the bureaucracy involved in credit analysis for other traditional payment methods.Also, the purchase in installments can be determined according to the most convenient period for the customer, such as weekly installments, for instance.

Advantages in Buy Now, Pay Later for users

The main advantages for customers when they choose the Buy Now, Pay Later payment method include:

- Purchase in installments for lower values

- Instant credit approval

- Less bureaucracy, no need to fill out a number of documents and wait a long time for a card delivery, for instance

- Purchases above a customer’s credit card limit

- Installment plan for those who don’t have a card

- Discounts at partner stores

- In general, either installments come without any interest or their interest rates are much lower than in credit cards or installment plans.

In addition to being a fast credit model, BNPL makes it possible to serve consumer profiles that tend to have difficulties in approving financing in the traditional way, as is the case of unbanked, self-employed professionals, students or unemployed people, for example.

Read also | Niche fintechs: The future of finances is built through inclusion and innovation

Advantages in Buy Now, Pay Later for retailers

On the other side of a transaction, retailers get the following advantages when they offer the Buy Now, Pay Later option:

- Increased sales numbers and new customers thanks to a new means of payment being offered

- Higher sales conversion

- Higher average ticket

- Risk in transactions is part of the financing party’s responsibility, not the retailer’s

- Full value is received at the moment of the purchased, after the BNPL enablement fee is deducted

- Improved customer retention

Read also | DeFi: Decentralizing finance is the next step

Advantages in Buy Now, Pay Later for companies providing financing services

For an industry made of companies providing financial services for enabling BNPL and fintech focused on that solution, the main advantages include:

- Capture of a new customer profile, which is young and unbanked

- Loyalty to a means of payment

- Adoption of the means of payment that most rapidly grows in developed countries

- Transactions with risk restricted to each operation

Read also | Financial API: Driving innovation in payments and banking

A means of payment on the rise: Understand the growth in Buy Now, Pay Later around the world

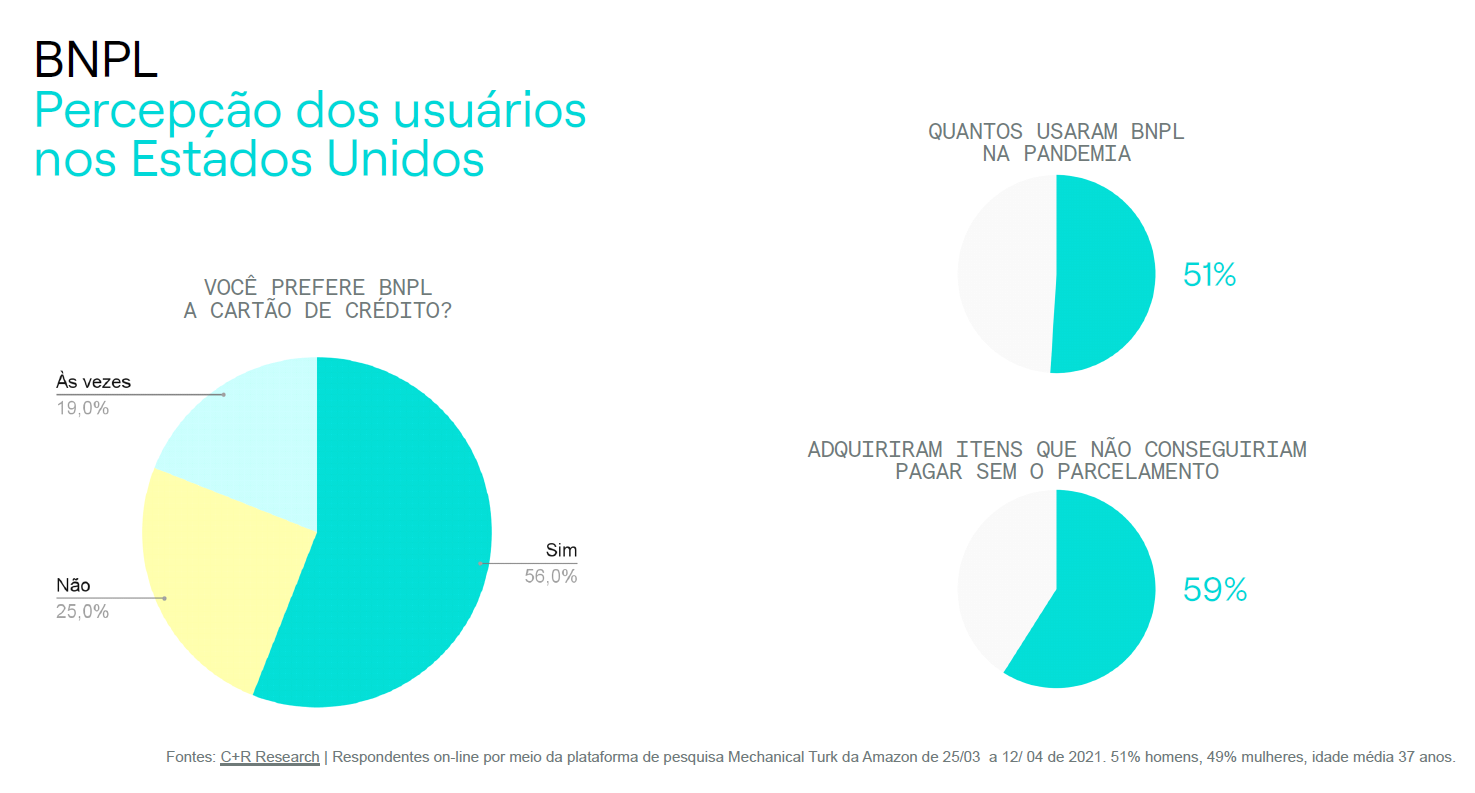

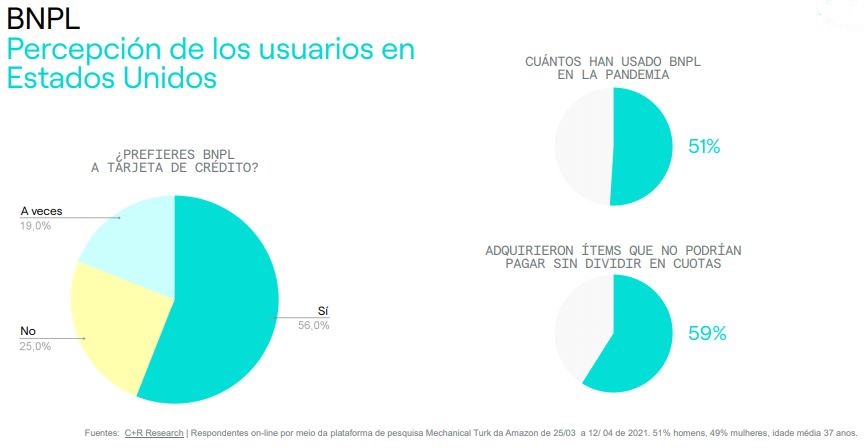

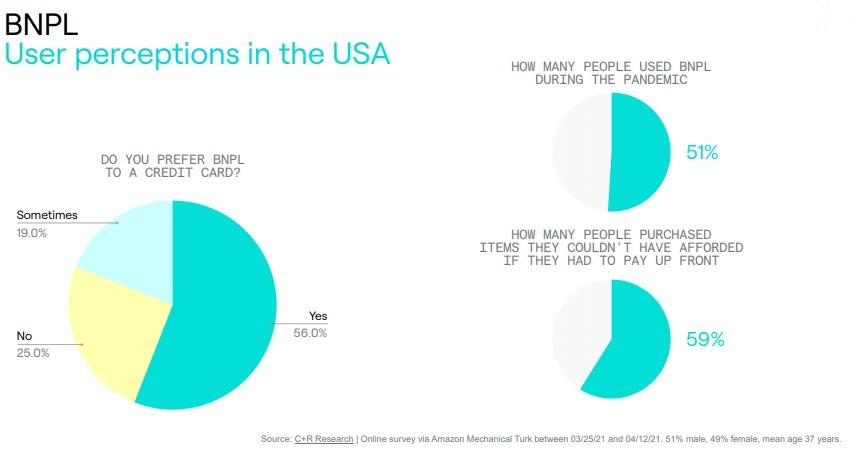

According to data collected by PYMNTS, BNPL is the fastest growing means of payment in developed economies such as the United States and European countries. Driven by the pandemic and the consequent growth of e-commerce, “Buy Now, Pay Later” has become more popular than other methods, such as instant payments and virtual wallets.

Such success is thanks especially to younger consumers. A study conducted by C+R Research has found that approximately 75% of BNPL users in the US are Gen Z or Millennials. Among Millennials, 26% used Buy Now, Pay Later solutions in recent purchases.

Attractive factors include the convenience in using that mode, which is fully integrated with the customer journey, without any credit analysis. BNPL can provide a higher average ticket for that group due to more stable finances associated with younger age groups and a lack of interest in acquiring credit cards offering high interest rates.

Experts at Kaleido Intelligence estimate that this means of payment will be responsible for moving 680 billion dollars by 2025. Keeping an eye on this industry, major players like Apple, Amazon and Visa have already released their own BNPL solutions, while a lot of fintechs and banks have also studied and released Buy Now, Pay Later solutions.

What about Latin America? Potential in Buy Now, Pay Later for the region

Although installments are more common in Latin American than in Europe and the United States, Buy Now, Pay Later hasn’t grown as expressively in that region. But why?

The popularity around installment-based methods in Latin America is especially thanks to factors like: low average purchasing power rates, economic instabilities causing unemployment, as well as enormous social inequality. In many cases, paying in installments in the only way for some people to buy more expensive goods, such as home appliances and electronics.

On the other hand, nearly 55% of the population in Latin America still doesn’t have an account at a bank (World Bank). That means that millions of people don’t have access to different means of payment that are not based on cash, such as pay slips (‘boletos’) in Brazil and vouchers in Mexico. In other words, although credit cards are quite popular, they are still inaccessible for a significant part of their audience.

Model takes baby steps, but shows great perspectives

Combined with an e-commerce growth driven by the Covid-19 pandemic, a significant demand has shown for means of payment that fill in two gaps: low banking rates for the population and the need for installments.

According to an analysis conducted by AMI, that’s why the BNPL model has the potential to capture 20% of online sales in Latin America.So, why is that growth still timid? ?

The first aspect to consider is that, even though countries in Latin America have some characteristics in common, they are not a homogenous block. There are nuances in cultural differences and buying habits which must be acknowledged and understood.

While in Brazil XNUMX% of the population does not have a credit card and the launch of instant payment system Pix it was a resounding success, in Colombia the most used means of payment even today by XNUMX% of the population is bank transfer. In other countries in the region, credit card remains the preferred method.

A second challenge for the rapid growth of “Buy Now, Pay Later” in Latin America is the need to develop technological and regulatory solutions that allow the intensive use of customer data Open Banking. After all, to enable BNPL's speed and flexibility, financiers need tools to instantly analyze credit granting, and sharing user data is key to that.

Read also | Open X: What’s next after Open Finance?

We’re keeping a close eye on the next step for financial inclusion

Financial inclusion for more than half of the population in Latin America won’t be beneficial for users merely from an individual standpoint. A payment mode like Buy Now, Pay Later can bring a positive impact for stimulating innovation and productive investments for economies in that region.

As a matter of fact, at Dock we believe that granting accessible, transparent credit is the next step for true financial inclusion after the boom in digital banks., transparent and affordable lending is the next step towards true financial inclusion.

Also, enabling financial services that don’t necessarily depend on traditional banks to be accessed—like BNPL doesn’t—is an excellent manner to empower that transformation. However, so that credit democratization actually advances, banks, technology companies and fintechs should work in collaboration in order to create a conducive environment for competition, which will contribute to developing the financial ecosystem in local economies.

Want to learn more about the scenario can evolve? Watch the talk by our CEO Antonio Soares at FEBRABAN TECH 2022:

Buy Now, Pay Later: Takeaways from this article

- Buy Now, Pay Later is a credit model that has been seen as a top trend in the credit industry. It’s also known as BNPL, which stands for Buy Now, Pay Later.

- BNPL is different from existing credit models, such as installment plans, since they involve a player granting credit, which reduces risk for a retailer.

- Buy Now, Pay Later is attractive especially for consumers who have difficulty in accessing credit in traditional models because they’re unbanked or don’t have a stable income, for instance.

- Although there’s been drastic growth in BNPL in the US and Europe, the model is taking baby steps in Latin America—and there’s great potential in it to contribute to financial inclusion.

Related articles

- Ley de Bancos in Peru: New regulation brings changes and opportunities for the financial industry

- BIN Sponsor Partner: What is it, and how does it enable new players in the means of payment industry?

- Credit industry in Latin America: 4 opportunities for driving the industry

- Retrospective for payments and banking in 2022: How did the industry grow in Latin America?