Open Data: Is it the future for Open Finance?

![]() 16 minutes reading

16 minutes reading

Have you ever heard about Open Data or Open Everything? Is it an evolved version expected from the Open Finance movement? Get to know what Open Data is in more details, how it is being developed in different countries worldwide and how it will impact your business.

After the advancement of Open Banking and its expansion to the model of Open Finance, world markets are dealing with an even broader movement: Open Data, also called Open Everything.

In this article, we will delve deeper into the concept to know the main challenges and opportunities that will certainly impact the market and the companies that offer products and services of banking e means of payment sector. Check it out!

What is Open Data?

Following Open Finance, Open Data is also a movement that is driven by the massive volume of data produced on a daily basis from continuous engagements between individuals and institutions around the world.

The core idea is the same: Each person is the holder of their information and can choose to grant access to it as a means to get benefits — whether for contracting new services, acquiring products or simply getting the appropriate customer service of any sort.

It is another information sharing movement, which enabled by new high-precision tools to refine data collected and generate valuable insights.

As Open Data advances, data collected and handled (commonly known as ‘smart data’) can also be used by other industries, such astransportation, energy, telecom, etc. Driven by an interest in such precious supply that is information, several industries are collaborating in order to spread and expand its access.

In a nutshell, Open Data aims to effortlessly enable data handling in robust, intercompatible systems. Institutions in all industries can share information through it to bring more convenience and efficiency to their audience.

As in Open Finance, obviously exchanging any element will only be possible if each individual expressly authorizes it — the power over it is centered around them.

Open Data importance: Why is it such a relevant topic?

A study conducted by Mckinsey Global Institute advocates that the expanded Open Data adoption will be able to cause significant, positive impact on GDP for major economies such as the United Stated, European Union and United Kingdom by 2030.

The estimated affect ranges from 1 to 1.5 percentage points in GDP growth for those economies, while it can reach 4 to 5 percentage points for India.

Such scenario shows that improving our data handling in financial services can be key to bring growth, competition and productivity to markets. It is also an interesting tool when dealing with economic crisis scenarios and can be used as a resource for governments.

Micro, small, medium and large-sized businesses in any industry will be able to benefit from the estimated potential of adopting Open Data. After all, as in Open Finance, those institutions can take numerous actions, including:

- Expanding their knowledge on each customer’s profile, avoiding fraudes;

- Improve your knowledge of each client’s profile, avoiding fraudare;

- Improve your knowledge of each client’s profile, avoiding fraudare;

- Targeting their marketing actions more accurately, improving their sales conversion rates;

- Improving human resource allocation according to demand in each location;

- Automating manual processes, creating value throughout the production chain;

- Ensuring access for more people in different product/service segments, etc.

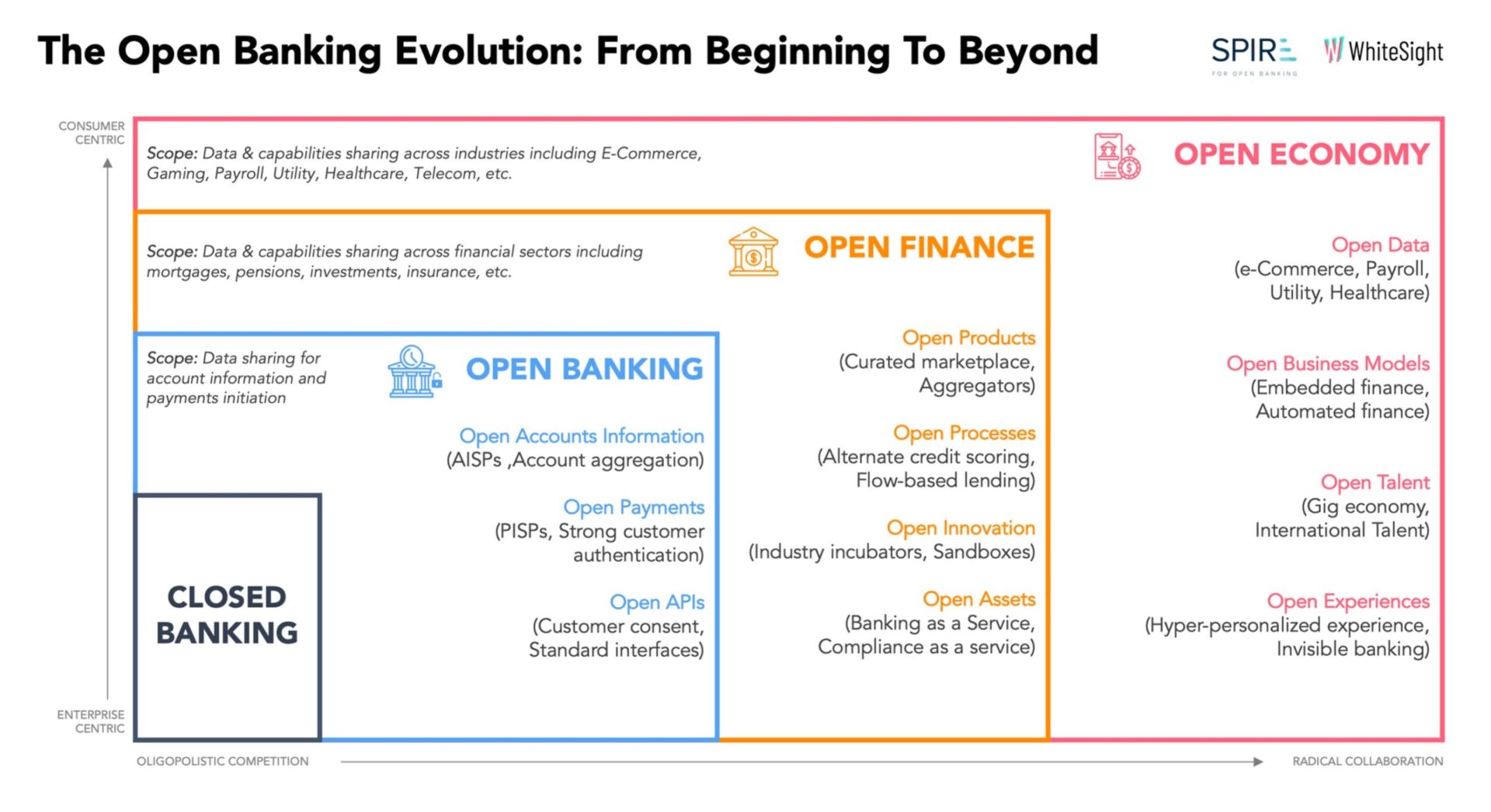

Open Data is part of a data opening context so that there is increasing collaboration among businesses to improve customer experience. Learn more in the WhiteSight’s infographic:

Open Data value for the payment and banking industry

Access democratization to customer financial history is likely to further increase competition in the industry.

Traditional, major banks, which have a significant share of the industry, will lose exclusive access to such valuable information — which means that this huge competitive edge over fintechs and other players will be beaten.

Therefore, information dilution among industry players is expected to be followed by a fierce race to enhance technological tools.

Keeping an eye on that trend, a lot of major banks have already looked to acquire or develop partnerships with startups and fintechs. It’s been one of the ways they found to stay competitive in developing modern apps and systems which are able to provide customers with more security and convenience.

If Open Finance already promised to revolutionize the financial industry, it’s safe to say that the impact caused by the Open Data expanded action will be even more pronounced. After all, companies in the industry will need to be equipped in terms of technology so that they can engage with companies in different industries.

Therefore, it is necessary to make sure that they will be able to have systems that are safe, fast and friendly enough not only to guarantee a good experience for your end customer as well as to enable interoperability with systems from other operating segments.

With Open Data, it is no longer “just” about sharing information to get benefits from accessing financial services and products. Now individuals and organizations will be interested in using the whole information history they have about themselves to achieve all kinds of advantage — even in healthcare, for instance.

Following the evolving debate on Open Data around the world is one of the best ways to get ready for that. Let’s get to it!

Open Data growth around the world

Several countries all around the world have started researching and discussing data governance and usability when it comes to Open Data. Here we provide the current overview of some of the top initiatives that have been adopted so far.

Open Data in the UK

A work group called ‘Smart Data Working Group’ in the UK signaled in 2020 the intention from the Government Administration to expand smart data initiatives to other industries. However, they have initially chosen to focus on well-regulated industries, such as financial services, telecom, gas and energy.

In their latest report published in 2021, the British work group revealed some of their conclusions obtained through case studies conducted in each of the selected industries. Opportunities and challenges being mapped and discussed will serve as a foundation to formulate appropriate policies.

Ah, it is worth remembering that the United Kingdom was a pioneer in implementing Open Banking in the world.

Australia and their first steps with Open Data

Australia has also chosen to start using Open Data in banking, telecom and energy industries. ‘Consumer Data Rights’ were implemented in 2013 as a form to ensure citizens had control over their data. The Australian Government partnered with research institutions and representatives of the industries involved in order to debate around artificial intelligence and machine learning.

In addition, initiatives from the Australian Government have focused on promoting law reforms to ensure data transparency without compromising their citizens’ privacy. It’s also been observed the need for adapting laws in order to enable inbound and outbound traffic for international information.

European Union and Open Data: How is the region dealing with it?

The European Union in turn has signaled the intention to further expand Open Data to industries such as manufacturing, energy, environment, agriculture, public administration, education, sciences and healthcare. Some recommendations have been announced on the topic in the document involving European strategies for data.

The European Union is expected to make strong progress when it comes to setting standards and building the appropriate infrastructure by 2030 in order to enable sharing the increasing volume of data that is produced on a daily basis.

It is only a matter of time until all industries are able to take part in it and benefit from sharing data securely and efficiently in general — and not only for companies, but also for individuals as consumers or citizens, as well as government agencies.

Opportunities created by Open Data

Inspired by the British model, Brazil adopted from the outset the expanded model of Open Finance, not restricted to banking institutions only, but encompassing all those that offer financial products such as insurance and investments.

It was also created General Data Protection Law - LGPD, a very important civil framework for data protection, establishing the main guidelines for obtaining, storing and processing information.

At the moment, the country is in the final phase of implementation of Open Finance, already in accordance with the LGPD, and by the end of 2022 the entry of the insurance segment (also known as “open insurance projects in place.").

The expectation is that once the adoption of Open Finance is finalized, research and discussions on Open Data will begin. Although the challenge is even greater, some important lessons will have been learned by then, which may facilitate the process.

In parallel, other initiatives to modernize the provision of financial services such as the revision of foreign exchange legislation to facilitate international payments and the adoption of the Pix, for example, have been implemented with support from the Central Bank.

Opportunities for the financial industry: See examples

Collectivizing access to data provided by Open Data will enable institutions in different fields to holistically and complementally analyze information. So it will get increasingly easier to acquire a deep understanding on each customer’s demand.

As a result, we can expect more customization in offering services and products, new opportunity windows for innovation, and more efficiency in pricing items.

The competition will depend on the use of intelligence in data processing.

The market tends to become more productive, competitive and secure. After all, institutions will have more information to prevent financial losses caused, for example, by the lack of information about the customer's real ability to pay.

With information about payment history, income, debts, housing, goods, consumption habits, etc., an insurance company, for example, will be able to customize its offer for the potential contractor. Your competitors will do the same, and the end customer will win, both in terms of price and in terms of satisfying their needs.

It is even possible that the dispute over the practicality of the services offered will gain more relevance than their price at the time of choice. This opens up even more space for new business models to be created.

Read too - Open X: What’s next after Open Finance?

Opportunities for the financial industry: See examples

Whereas Open Finance is expected to provide significant gains for customers and companies when it comes to accessing general planning and financial services, Open data may provide even more benefits. Check out some examples below.

Car shops or brokers will be able to ensure a higher sales conversion rate by studying their potential buyer’s information history, such as daily transit, income, payments, previous leases or mortgages, household income profile, etc. Thus, the company can guide them through a more customized shopping experience that is appropriate to their needs.

The associated financial institution in turn will also have access to the information in order to provide conditions that are appropriate to the buyer’s actual payment ability, while considering the goods to be purchased, fees, terms and conditions that are appropriate to that customer and wouldn’t be feasible without the same level of detail.

Insurance companies will be able to make payments for compensations that are due to the contracting party without the need for the customer to provide proof. The bureaucracy for proof can move directly from the insurer platform to the airline platform in case of a travel insurance, for instance.

The more comprehensive use of the huge volume of data produced will also enable new financial tools to be built. For example, apps that automatically cancel subscriptions for services that are not often used, if they communicate directly to the platforms that are responsible for those services.

Moreover, it is possible to map banking information in order to understand an individual’s behavior along the month and detect the most appropriate moment for a custom offer.

Do you want to check more opportunities to move society forward with Open Data? Watch the TED Talk on use of open data in the public sector:

Roadblocks to take into account: Main challenges in Open Data

Possibilities are endless, and gains are promising. However, some important challenges need to be addressed so that Open Data becomes a reality.

One of the main roadblocks related to the global Open Data expansion involves regulation. As in Open Finance, it is necessary to consider the formulation of strong rules to ensure privacy and security for individuals whose information one wishes to share — inside and outside their country of origin.

The need for express consent from each person partially addresses the issue, but it is not enough. There has to be clarity on what will be shared, the purpose of its use and potential consequences. Besides, regulations need to be continuously reviewed and updated so that they can keep up with technological advances and international laws.

Another issue that causes apprehension in discussions — especially in the United States and Europe — is that data accumulation might be used by major technology enterprises to monopolize markets.

After all, although the expectation is precisely to increase competitiveness, it is necessary to create laws that prevent serial mergers and acquisitions, especially by large organizations interested in access to technology and databases of smaller companies.

There is also an ethical issue that is relevant to be considered in relation to the possibilities Open Data brings. In the UK, a study has showed that public opinion on sharing health-related information remains controversial.

There is some apprehension over companies accessing people’s health information and causing a negative impact on their lives — whether for exclusion in job recruitment processes, increased cost for healthcare, insurance or loan services, for instance.

Finally, it is also worth mentioning the big technological challenge to be faced. The wide information transmission provided by Open Data requires organizations to operate from intercompatible platforms in continuous improvement for maintaining security. Companies from different industries will need technological infrastructure to enable their interoperability.

Read too - Invisible banking: Invisible finances are more than a ‘futuristic’ trend

One more step for evolving banking and means of payment

As we mentioned in this article, Open Data implementation has promised to revolutionize many industries in our economy, going beyond the financial industry. Many opportunities for innovation will arise from enhancing technology platforms that are used and maturing regulations that have been formulated and adapted.

Here at Dock, we’re following all that movement and its opportunities, which will help democratize financial services!

Main takeaways from this article: What is Open Data and its possibilities?

- Open Data is a model for data sharing, when authorized by their holder, among companies and organizations in different industries in order to provide better experiences and services.

- Open Data will connect industries such as financial services, transportation, energy and insurance, enabling data to be used in developing more customized and affordable solutions based on the customer’s relationship history from another industry.

- The Open Data model is part of a larger context that has first started with Open Banking and evolved to Open Finance — both in implementation stage in many countries.

- Some countries and regions have projects for Open Data, including the UK, Australia, European Union and Brazil.

Related articles:

- Building a digital bank: The ropes for businesses looking to get started on this journey

- Trends in the financial market: six highlights from the Tech Trends Report

- Buy Now, Pay Later: a model with huge potential in Latin America. And opportunities for your business!

- Cryptocurrency security: how to go crypto without getting caught out