Agritech: 5 opportunities for innovating in agribusiness by relying on financial solutions

![]() 10 minutes reading

10 minutes reading

The agribusiness industry is a major pillar for economies in Latin America, showing great growth in the past few years. And technology plays an important role in that scenario through businesses known as agritech—which serve as a bridge between the industry and highly specialized solutions.

Taking Brazil, as an example—a leader in exports for agriculture and livestock farming products in the region and the 4th in the world—, studies conducted by Center for Advanced Studies in Applied Economics (Cepea)and CNA (Brazilian Confederation of Agriculture and Livestock) show that the GDP for the Brazilian agribusiness industry grew by 8.36% in 2022. Argentina and Mexico are also leaders in the industry and ranked among the top producers in the world.

Those numbers are impressive and also indicate that the industry presents a great opportunity in terms of target audiences for companies looking to provide a variety of services. After all, agribusiness is a huge industry, but there are a lot of pipelines when it comes to a credit market for specific technologies and producers at farms and crops.

The good news is that there’s increasingly more space in the current scenario for providers and players looking to explore that opportunity—and that’s where agritech comes into play. Learn more about it in this article!

What is agritech?

Agritech—or also agtech—is basically a startup providing technology solutions designed exclusively for agribusiness.

In other words, agtech can be seen as an initiative aiming to bring and drive technological innovation for agriculturists (from small producers to large farms) by streamlining access to credit and tools that are able to automate and accelerate productivity in rural areas.

What are the existing types of agritech?

Companies falling into the agtech category are able to work with different fronts in agribusiness by offering technological tools and resources that take into account industry specificities—which can range from building financial solutions to developing technologies that help automate their supply chain, contribute to minimizing waste and enable them to market supplies digitally.

We’ve curated some of the most important types of agritech in the list below:

Agritech specialized in consuting services

Startups focused on small and mid-sized agricultural producers. It consists of a comprehensive line of work and can comprise extensive fronts, such as analyzing levels of production, identifying pipelines or risk factors preventing expansion and, finally, studying sustainable planting and harvesting techniques that don’t damage the soil. As a consulting actor, agritech is responsible for collecting that data, building an action plan and working closely with clients.

Agritech developing software for agricultural management

It offers integrated control over different parts of the job in a farm: asset and finance management, harvest control, personnel monitoring, harvesting balance, technical project budgeting, and more.

Agritech working with solutions designed within the Internet of Things (IoT) architecture

Since we’ve already mentioned agricultural management, why not go beyond and offer an agtech solution to change your operational structure for farms and crops? The Internet of Things can be a powerful partner for agribusiness by precisely estimating the best harvest dates, calculating levels and spendings on supplies, collecting weather data and helping create a truly connected environment.

Agtech relying on precision agriculture solutions

Precision agriculture is a term used for identifying an entire set of technologies collecting geographic data on crops and monitoring planting and harvesting techniques, so that companies can offer a more integrated scenario between the producer’s soil and goals.

Agri-fintechs, the fintechs in agribusiness

Offering solutions in banking, cards & credit for agro companies, independent rural producers and other people and businesses connected to this ecosystem (which includes, for example, digital account, credit card processing instant payments and release of customized installment plans for the sector).

5 opportunities for innovating in the agribusiness industry by relying on financial solutions

If you already have a company that offers financial services, are in agribusiness or are thinking of exploring the financial world through models such as Banking as a Service, it is worth knowing some of the main opportunities in fintech agro:

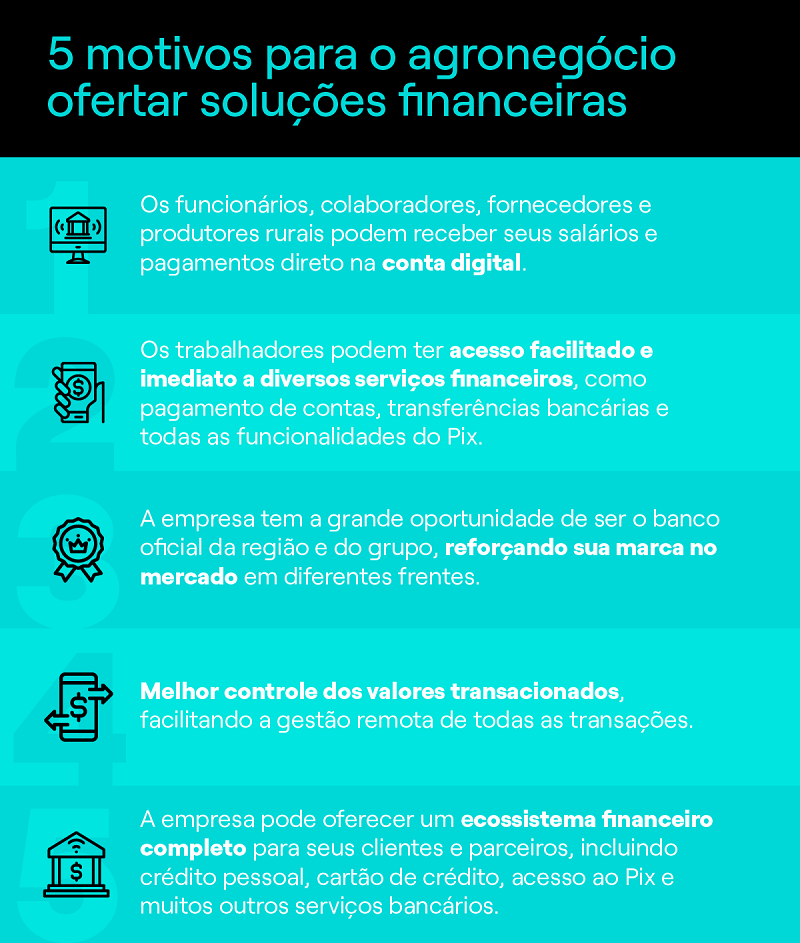

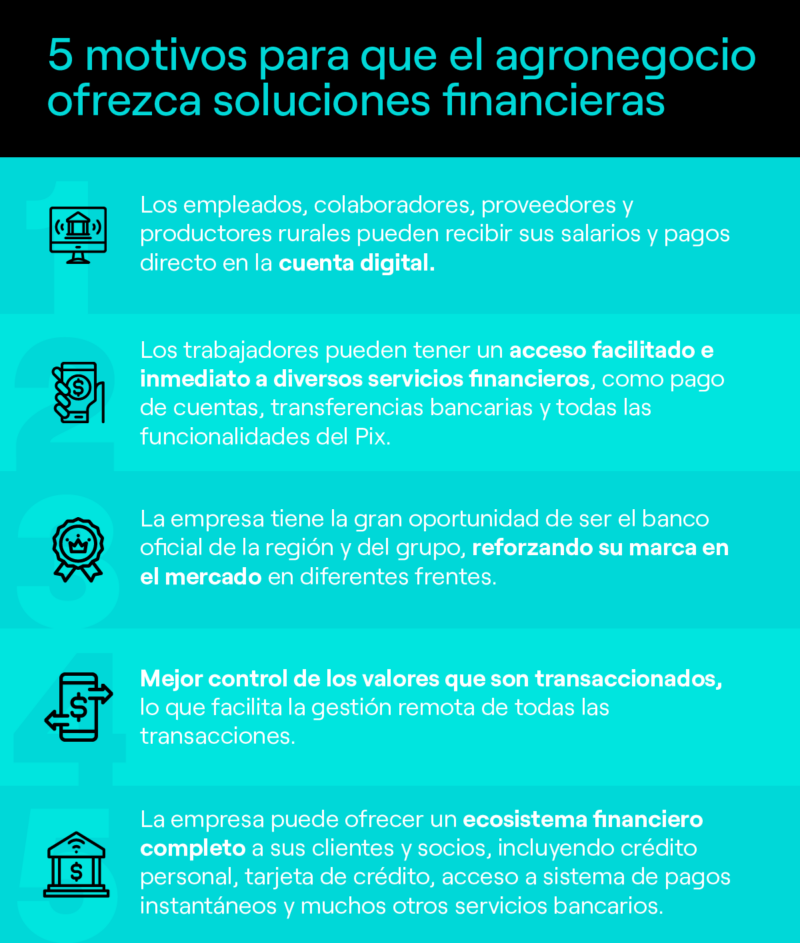

1. Engaging the production chain by leveraging financial solutions

With an agrotech specialized in banking, it is possible to open digital accounts for all employees, collaborators, suppliers and rural producers of a company or producing region. These people can receive their wages and payments directly into a digital account, simplifying transfer processes and even access to credit cards and debt.

2. Driving results through credit

An agri-fintech capable of ensuring a reasonable operation area (or partnering with an important group in agribusiness) has a great opportunity to become the official bank in the region and/or group. That means a stronger presence in the market as a whole and the ability to attract not only more clients, but also more investments in new products.

3. Engaging an unbanked audience by leveraging financial solutions

A banking agtech can provide rural workers and producers with quick, easy access to different means of payment , thus helping bank a customer profile that still doesn’t have access to the traditional financial system or underutilizes it.

4. Building a complete ecosystem

With a complete digital banking solution, a fintech agro startup can build aecosystem complete financial services for its customers and partners, including personal credit, credit card and several other financial services.

5. Having better management control

A detailed, end-to-end view of values in transactions is essential for any player in the financial industry, but it is even more important within banking agtech—which deals with different fronts, such as marketing supplies, paying agriculturists, offering personal credit lines, adjusting prices for final consumers, handling supply chains and harvest cycles, and more. That’s why it is easier to manage all transactions remotely by having better control over those values.

Agri-fintech: What are the challenges?

The fintech agro concept stands as an alternative to financial institution more traditional, as it prioritizes accessibility and banking of people and families who live from agricultural production, as well as the delivery of services that really meet the demands of this market.

Although the agri-fintech industry is growing, and there are different opportunities for companies looking to offer digital bankingplatforms, it is also important to draw some of the main challenges that type of startup can face.

The data below was curated based on a recent study conducted by AgTech on the agritech scenario in Brazil, which shows similarities with other countries in the region:

- Beyond the Southeastern region: 62% of agritech startups are based in São Paulo and Minas Gerais, which means that agtech solutions haven’t solidified their presence in other regions of the country. Agribusiness producers are also based on several different states that can benefit from more localized solutions.

- Lack of connectivity in rural areas: robust blockchainsolutions, financial platforms, harvest forecasts based on artificial intelligence, intelligent plague control, and more. It all seems amazing, but it is only possible thanks to the Internet. And unfortunately, not all agribusiness regions have reliable Internet connection. 5G is expected to take digital inclusion to rural areas.

- Lack of third-party investment: partnering with third-party companies and ensuring more significant investments is a major difficulty for agri-fintechs, since the negotiation time for those players is usually long.

- Lack of women in the agtech universe: the presence of women in tech is historically low, but that is a serious issue for agritech—also because 64% of Brazilian agtech startups have none or only one woman as a team member. That scenario is not favorable for inclusivity and, unfortunately, doesn’t shed light on potential talents available for the industry.

Here at Dock, we believe that strengthening the ecosystem of fintechs focused on an agribusiness industry that contributes to their growth is what it takes to overcome those challenges and incrementally accelerate financial inclusion in rural areas and economic development for producers.

How can Dock help your agritech with financial services?

With our global platform for banking and payment, we contribute so that banks, fintech and companies from different industries can provide complete financial solutions.

While your agri-fintech focuses on customer experience and product development, Dock takes care of the technological and bureaucratic issues so that your business can grow and change lives in rural areas.

Want to learn more? Learn about Dock One:

Agrotech: summary

- Latin America is a powerful agribusiness market, and there’s a lot of space for small and mid-size providers and players looking to offer technological solutions customized for the industry—and that’s where agritech comes into play.

- Agrotech, or agtech, is a startup aiming to bring and drive technological innovation for agriculturists by streamlining and accelerating agricultural processes in rural areas.

- There are several types of agtech, but one of the niches showing the highest potential is agri-fintech, which provides banking services.

- The main challenges in agritech are: lack of connectivity in rural areas, low third-party investments, lack of women in the workforce and little presence beyond the Southeast region in Brazil.

- There are 5 ways for an agritech startup to innovate in the banking industry: engaging their production chain by leveraging financial solutions; driving results through credit; offering a complete banking system; having better management control.

Articles related to agrotech:

- Financial inclusion in Latin America: The scenario and opportunities for fintechs

- Financial inclusion and fraud prevention: How does security in payments contributes to new advances?

- Beyond Banking: How banks and fintechs go beyond the basics and attract clients

- Ley Fintech in Chile: A promising scenario for the industry and growth towards financial inclusion