Neobanks: A growing industry playing an important role for accessing financial services

![]() 15 minutes reading

15 minutes reading

Neobanks are financial institutions reinventing the way clients and organizations in the financial industry connect across the world. By innovating and facilitating access to services and products, these digital banks play a relevant role in financially including the population in Latin America.

You’ve certainly heard about the term ‘neobank’. In fact, that concept is expected to get increasingly popular as the number of financial institutions of that kind has been continuously growing in the past few years.

Many businesses find the format a great opportunity to enter the financial ecosystem. And, by focusing on uncomplicating solutions and facilitating access to different services, they bring countless benefits to users, contribute to the evolution of the market and play an important role in Financial inclusion of the unbanked population.

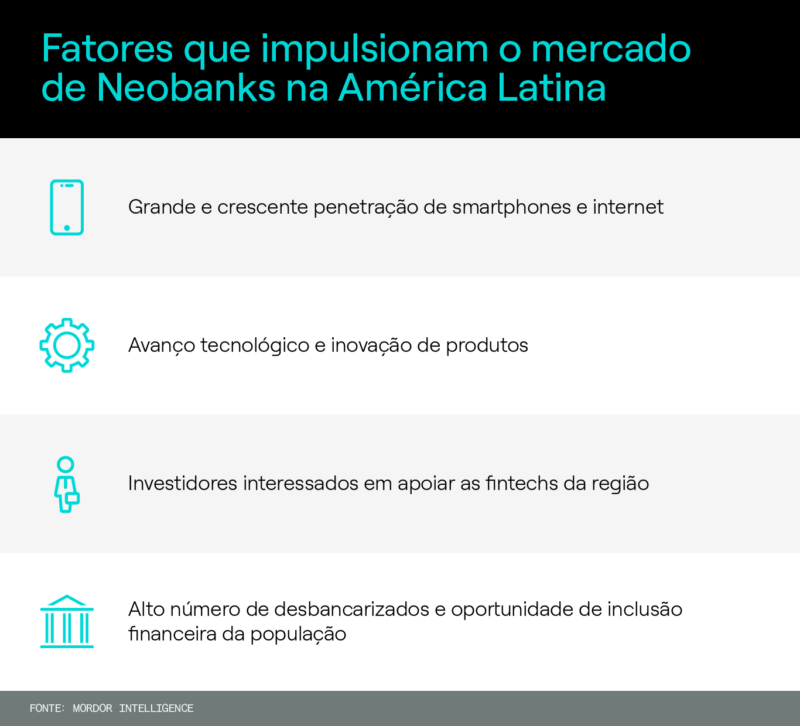

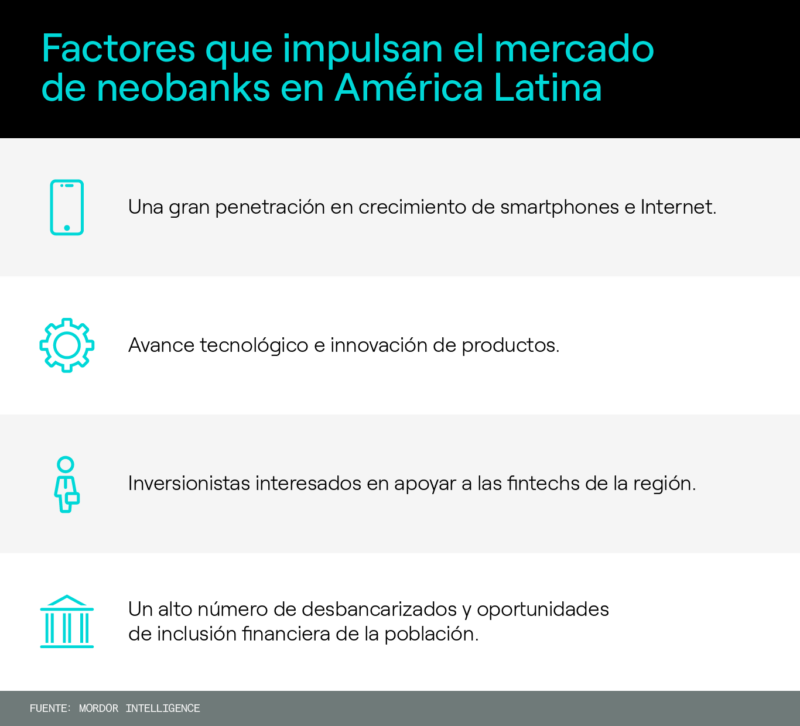

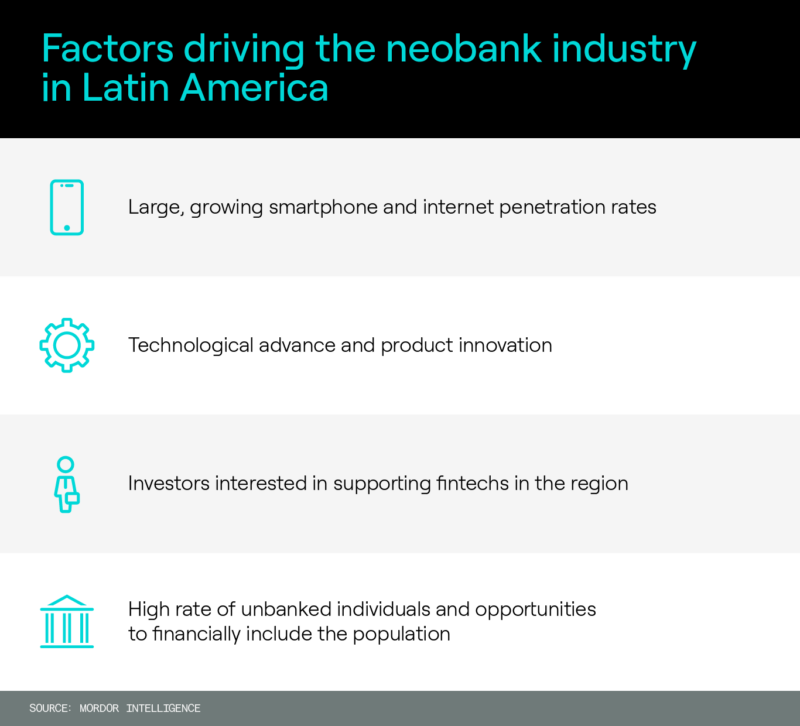

While neobanks grow around the world, they have gained special momentum in Latin America, a market full of opportunities and people in need to be financial included.

But what are neobanks?

Neobanks are financial institutions based on technology—without a physical branch and with a 100% digital operation —and platforms enabled through websites and apps. They usually focus on providing basic financial services for their clients, without bureacratic procedures and reduced costs.

"Digital banks” and “neobanks” aare concepts commonly used as synonyms, since both institutions extensively leverage technology and innovation to understand and meet industry demands, especially for the population that’s still unbanked.

However, an important difference between a neobank and a digital bank is that the digital bank is sometimes linked to traditional banks or bank holdings. The most frequent use of the term neobanks refers to fintech totalmente independent.

In other words, restrictively speaking, it’s possible to say that not all digital banks are necessarily neobanks, but all neobanks are digital banks.

The role neobanks play in driving financial inclusion

Since a main goal for neobanks is to focus on the population still lacking access to financial services, they mainly concentrate their efforts in streamlining banking procedures, facilitating access to basic services and products and communicating clearly and assertively.

The strategy has stimulated many unbanked, that is, people with no history of relationship with banks, to open an account for free via cell phone, without bureaucracy, without cost and very quickly.

Neobanks benefit their users, market and economy

Thus, in addition to playing an important role in promoting financial inclusion in Latin America, neobanks respond to a demand that is very present in the current scenario: the need to make things simple.

So apart from having an important role in promoting means of payment industry and economy as a whole—which is very important given the Latin American context.

For the population

The main benefit neobanks bring for the population is making basic banking services more popular. After all, neobanks offer:

- less bureaucracy for opening an account: less documentation is required, everything is online, so the process is simple and quick;

- no charges or lower fees and commissions for basic services: since they present reduced operational costs, with no need to maintain the physical service structure, neobanks can also enable savings for their clients;

- cashback: neobanks usually provide a percentage of cashback for clients using their products and services, which is another attractive aspect for the population;

- marketplace: some neobanks also have a digital marketplaceavailable, where clients can shop and take advantage of exclusive benefits and better conditions.

For the banking and payment industry

Neobanks’ penetration drives more competition and diversity in the financial industry. Mid- and big-sized traditional banks, which used to take a significant portion of the industry, now need to deal with positive, innovative competition—generating more gains for their clients.

Neobanks encourage people to stop using cash and start using new means of payment, that is, the most modern services provided by the platforms. This stimulates innovation and, consequently, the evolution of the sector.

What’s more, emerging neobanks can represent a profitable and strategic opportunity to expand business operations to different segments. Even consolidated businesses in different industries like retail, for instance, have noticed that having their own neobank can further drive their sales, deepen knowledge on their consumers and diversity their sources of revenue.

For the economy

By facilitating access for a new population group—mainly unbanked individuals—neobanks contribute to the economical development, while also promoting a growing banking and means of payment industry.

Apart from creating new jobs and fostering a local productive chain, people that weren’t financially included now have access to and leverage different products and services.

Also, as that population is financially included, the use of means of payment, for instance (such as digital wallets and BNPL (Buy Now, Pay Later), for example, be even more accelerated. Thus, a larger part of the population also has access to credit and loans, which helps to move the economy even further.

Neobanks across world

As much as the social isolation caused by the Covid-19 pandemic has greatly boosted the use of digital banks and means of approach payment (contactless), the neobank market is still small in several regions of the world.

Nowadays, the region showing the highest neobanks’ penetration rate is Europe, which effectively promoted the regulatory changes required to develop those institutions.

In the US, data collected by InsiderIntelligence show that there’s still significant space to expand the use of neobanks: there are 24,9 million account holders today, and that number is expected to grow to 2025 million by 39,1.

Growth in Latin America

The surprise lies in Latin America: although there’s still a lot of space to grow, the market in the region has seen exceptional growth for local neobanks.For the Latin American audience, the main attractive aspect in neobanks and digital banks is lower costs, 24hs availability and quick transactions.

In 2021, there were over 30 existing players in Latin American countries, serving around 11% of the total population in the region, which represents over 50 million clients according to a study conducted by Fincog, a strategic consulting agency specialized in fintechs.

According to a study by Mordor Intelligence, the top 10 digital banks in the region are responsible for over 90% of all neobank clients in Latin America. However, the market is full of opportunities and in expansion.

Neobanks in Brazil

According to a study conducted by Rapyd, out of all Latin American countries, Brazil shows the most receptive audience in the region when it comes to digital proposals such as neobanks and other fintechs.

Compared to their neighbors, Brazilians are the most willing to leave traditional banks or even open accounts at more than one bank—83% of the interviewed individuals in the study.

That trend was also evident in the analysis promoted by Bank of America. Still in 2021, the number of active users a month at digital banks already surpassed by 15 million the number of active users at traditional banks. In addition, 19% of Brazilians are estimated to exclusively have a digital account, according to data made available by Instituto Locomotiva.

More recently, GlobalNeobankingMarket and Trends 2023showed that Brazil is a world leader in terms of neobanks. The number of fintechs (including digital banks) has had a continuous annual growth rate—almost 3x higher between 2017 and 2021 in the country.

According to the same study, Brazil has one of the highest rates for exclusively digital account adoption, which would represent almost half of the adult population in the country.

Although the temporary emergency financial assistance program in the country during the Covid-19 crisis has contributed to banking a significant part of the population, another significant part still doesn’t have a bank account. It is actually an important audience lacking access, which will be benefited by neobanks to emerge.

Neobanks in Colombia, Mexico, Chile and Argentina

While leaving traditional banks doesn’t seem to be a big deal for the majority of Brazilians (83% of the interviewed individuals), the same is valid for most of the Latin Americans in different countries: in Colombia, 67% and Mexico, 65% of the interviewed individuals answered similarly. The most divergent scenario is seen in Argentina , where only 34% shared the same view.

Although neobanks’ penetration is moving more slowly in those countries, the scenario for growth is promising across Latin America. It is estimated that almost half of the population doesn’t have a bank account, and an even lower percentage has access to credit in the region.

The excess of bureaucracy associated with inadequate documentation for the lower-income population are commonly faced obstacles, as well as the difficulty in transportation from remote areas to physical branches for customer service.

Keeping an eye on that gap to fill, some important neobanks have started operating in:

- Mexico: the country is the second most promising market in the digital bank segment, while Brazil is the first. It is worth mentioning Klar, which offers credit and debit cards that can be contracted within 3 minutes at 1% of cashback, free of charge. Within a year, Klar captured 1 million new clients and made 1,4x more revenue.

- Colombia: important to mention Nequi, with over 10 million users making over 500 thousand transactions daily.

- Argentina: Brubank reached the mark of 2021 million users in 1,5 and already plans to expand to more countries.

- Chile: created in 2017, it took Mach only 2,6 years to become the second largest financial institution in number of users in the country: XNUMX million.

Financial innovation in practical terms: success cases of neobanks

To illustrate what we’ve covered so far, we’ll discuss two examples of Brazilian neobanks leveraging financial innovation to achieve huge success and contribute to financial inclusion within few years in operation.

Neon

Neon was founded in Brazil in XNUMX with a single product: digital account. Slowly but surely, their range of products expanded and started offering personal loans, credit card and some investment options.

In order to attract more users, Neon has developed free tools for financial education content in their app, which has helped their clients save and invest their money, by combining it with transparency in their communication with clients. They achieved such success that in 2022, this Brazilian neobank reached the mark of 22 million people in their customer base..

Two strategies should be emphasized when it comes to results achieved by Neon:

- Continuous effort to release free and innovative tools for their clients to use and access their basic products.

- Special attention to have an advantageous position in specific niches, such as the one for micro-, small- and mid-sized businesses. To that end, they released Neon Pejota, featuring a digital account for legal persons to serve specifically the needs for small business owners (MEI and ME) at a lower cost than the market average.

C6

Founded in Brazil in 2019, the neobank C6 mainly focused on offering free basic services along with more sophisticated options in one app. Back then, few competitors offered that level of convenience; it was common for clients to use more than one app.

CXXNUMX also leveraged a strategy based on diversifying their range of products. It was the first neobank in Brazil to offer a toll tag free of charge and enable an international bank account in Euro. Up until that point, that type of product was exclusively offer in private-label banking.

As a result from all that effort, C6 surpassed the mark of 20 million clients in 2022.

How to build your neoback more quickly?

Building a neobank has become part of the expansion strategy for many existing consolidated companies in their own industries — not only for diversifying their portfolio, but most of all for increasing customer loyalty and capturing. Customer Loyalty.

However, a main difficulty in quickly building a digital bank is the time required to develop an appropriate technological platform as well as all regulatory issues to get started. The time required to deal with all those points can force companies to miss important opportunities for gains in the industry.

To solve that issue, Dock has developed the ideal product: white label digital bank, which is a highly tailored banking platform based on cutting-edge technology and a quicker time-to-market. time to market much faster.

No matter what your entrepreneurial venture is, you can tailor it so that it has your look and feel and meets your clients’ specific needs. Through it, neobank users can:

- pay bills;

- make instant payments;

- make wire transfers;

- generate pay slip;

- make prepaid phone charging;

- issue vouchers;

- contract personal loans;

- open an interest-based account.

See more details on Dock’s banking platform below:

With a white-label digital bank, deploying neobanks is quicker and easier. Also, the partner company can focus their efforts on capturing new clients or working on their main activity. After all, all regulatory, treasury and new product and service development issues are part of our responsibilities.

Want to learn more about Dock’s banking platform? Click on the image below:

Neobanks: Takeaways from this article

- Neobanks are institutions leveraging technology and innovation to meet industry demands—without a physical branch and with a 100% digital operation.

- Neobanks focus their efforts mainly on simplifying procedures, facilitating access to financial products and more basic services and uncomplicated and assertive communication.

- Thus, they contribute to driving financial inclusion, especially in regions showing that demand, such as Latin America.

- Neobank clients benefit from less bureaucracy, lower costs and a quicker and more streamlined process.

- Building a neobank can represent a profitable and strategic opportunity to expand business operations to different segments.

- Many neobanks have emerged in Latin America, especially in the Brazilian market, with success cases such as Neon and C6.

- Dock’s highly customizable banking platform is based of cutting-edge technology and enables businesses to quickly build neobanks.

Related articles:

- Embedded Finance: The phenomenon turning companies into ‘banks’

- Web3: Understand what it is and the changes it can bring the financial industry

- Agritech: 5 opportunities for innovating in agribusiness by relying on financial solutions

- Financial inclusion in Latin America: The scenario and opportunities for fintechs