Digital accounts: your company can offer financial services too

![]() 15 minutes reading

15 minutes reading

The digital revolution transformed access and use of financial services all over the world, particularly in Latin America. Although cash has been the main way of making and receiving payments for a very long time, today we see the digital account taking this leading role. This not only provides a better experience for the consumer; it is driving financial inclusion, and creating opportunities for companies working in a wide variety of sectors.

Not too long ago, when we talked about accounts for financial transactions, we thought about banks and mainly large institutions. The Brazilian market, for example, has always been recognized as having one of the largest concentrations in this sector worldwide.

However, this scenario has been changing. According to the Economic Banking Report from the Central Bank, in 2021, the five largest Brazilian banks represented nearly 76% of the financial market in the country. In 2012, that index was 81%.

That drop in banking concentration is closely linked to the appearance of fintech and their digital accounts, which quickly engaged consumers and increased competition in the sector. As the World Bank’s Global Findex 2021research shows, two-thirds of adults worldwide now make or receive digital payments.

However, one would be mistaken thinking that it is only the banks – traditional institutions or digital banks.– that are offering this digital experience. The truth is that companies from different sectors can become payment institutions. Maybe yours can be one too!

What is a digital account?

A digital account is very similar to a traditional account. It’s as if it were the digital version of the bank account and the services available in a physical agency. Thus, its principal characteristic is that it is operated mainly online, whether through an application or on the institution’s site.

In general, digital accounts are offered by fully digital financial institutions, although some traditional banks have started offering this alternative in recent years.

How does a digital account work?

In a digital account, the majority of the transactions – if not all – are handled online. This allows processes such as opening and closing an account to occur more quickly, practically, and with less bureaucracy in comparison with traditional bank accounts.

The functionalities of a digital account vary according to the institution, but as a rule, payments, withdrawals, deposits, transfers, and cell phone recharges, among other transactions, can be made.

For example, it is normal for some digital accounts to offer online purchases within the application, as well as cashback programs, loans, and even investment options.

TV Brasil recently ran a story on the ease of digital financial solutions digital:

The role of digital accounts in financial inclusion

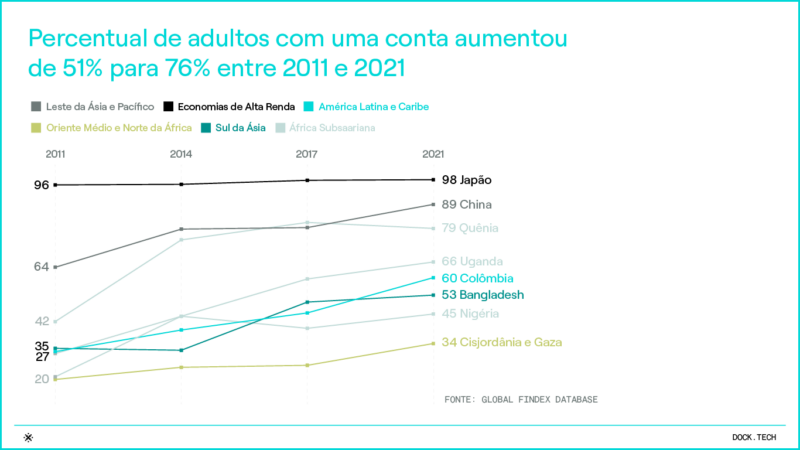

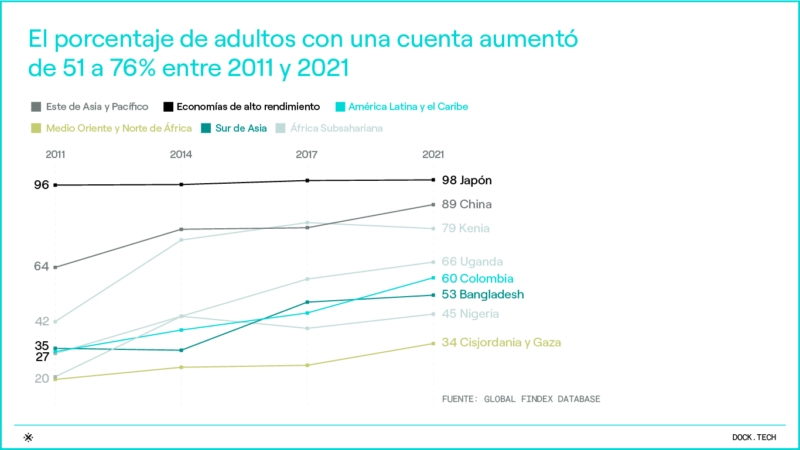

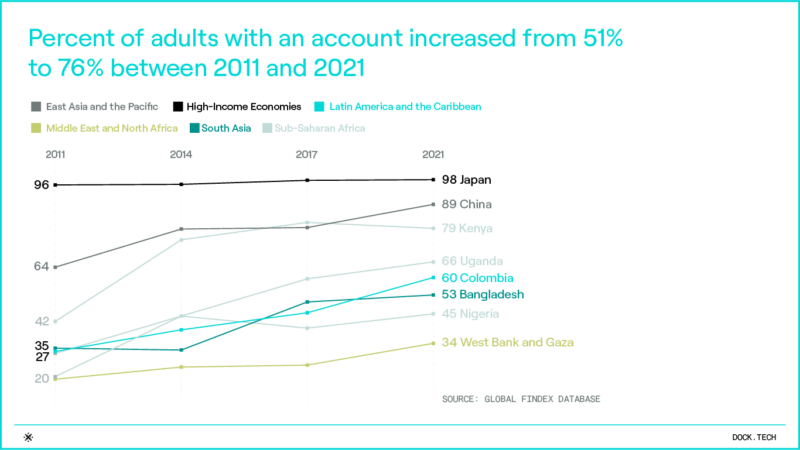

When we talk about digital accounts, we are also talking about financial inclusion in Latin America for a significant portion of the population in the region. According to data from Global Findex XNUMX, XNUMX million people are considered to be unbanked in Latin America, that is, they don’t have access to services such as bank or savings accounts, debit cards, or credit cards.

When companies assume the function of offering digital accounts to the public with whom they already have a relationship of trust, it is possible to contribute to transformation in this area. This happens both with the elimination of any barriers (physical, to open an account at a bank branch, for example), and by reducing costs for the user, with free or lower-rate transactions.

With financial inclusion, consumers also have access to various digital services, such as the use of transportation, entertainment, and food applications, among others. And we haven’t even touched on the means of payment technologies that enhance business, such as tap to pay, biometry and instant payments.

The advance of digital financial inclusion in Latin America

It is undeniable that digital financial inclusion played an important role in the coronavirus pandemic, lessening the impacts of social isolation.

As the aforementioned study states, Latin America and the Caribbean were the regions of the world that advanced the most in terms of inclusion: the proportion of adults with a bank account increased 18% over 2017. In 73, 2021% of adults had a bank account, and 14% of adults made a digital payment for the first time during the pandemic.

Brazil is one of the standouts in the region in relation to the digital inclusion movement, given that the opening of accounts through digital channels in 2022 exceeded physical channels for the first time in Brazil, as stated by the 30th Febraban Report on Banking Technology.

![]()

![]()

![]()

What are the advantages of a digital account for users?

It’s a fact that in recent years digital bank accounts have become more and more popular among consumers. And no wonder: after all, a digital account offers countless advantages over traditional accounts, both for the user and for the institutions that provide the accounts:

- Low or non-existent fees: digital bank accounts have lower operating costs, therefore they have lower or even no fees, as compared to traditional banks.

- Simplified opening process: the procedure can be completely online and with less bureaucracy.

- Simplified access to bank services: financial transactions are through the app, while the majority can take place at any time and in any location.

- Security: most digital bank accounts have fraud prevention solutions, combining the most up-to-date solutions to maintain a balance between prevention, data privacy, and client experience.

- Attractive investments: many digital accounts also offer the possibility of making a series of investments that can be accessed through the application.

- Integration with other platforms: digital accounts can also be integrated with other platforms, such as payment applications and digital wallets, which makes transactions even simpler and more agile.

Beyond banks: sectors and types of companies that offer digital accounts

What models are used to offer digital accounts, and to whom? The answer is simple: it depends on the profile of your business and your target audience. Hand in hand with clients and the means of payment market in recent years, we have developed and understand success models, which we share below. Do any of these make sense for your company?

Retailers

Companies Retailers companies lead the way in offering digital accounts. Among the reasons for this is the high volume of clients whose loyalty can be gained through financial services, in addition to proximity with these people, who have trust in the vendor at points of sale.

As most major retailers already offer private label cards or concession services credit, the migration to a digital account represents an evolution in the financial products available to customers.

A good example is the digital account of a fashion retailer, a pioneer in private label cards in Brazil, which assumed management of its financial productsin under one year, reaching two million clients and raising the average sale by 25%.

Applications

Applications for different types of services (delivery, transportation, food, entertainment, etc.) are evolving so they can provide their own digital wallet to clients, both to pay for transactions through the app, and to pay bills, to have basic accounts, and to recharge cell phones, among other services.

This is a way of simplifying transactions, while at the same time offering exclusive benefits such as vouchers or cashback, with the main objective of gaining user loyalty.

Perhaps you already know about and even use a digital account under this type of model, such as RappiPay, which offers 3% cashback on transactions such as credit card purchases, bill payments, and transfers to other people

Companies with outsourced sales forces

By creating digital accounts, organizations that have an outsourced sales force of resellers or commercial representatives not only facilitate financial relationships with these intermediaries, they also give the end consumer access to more modern means of payment.

A digital account can be provided to the sales force, allowing payment links to be generated and sent, without having to invest in card terminals, for example.

This is what happened with the leading cosmetics company in Brazil which, when it banked the direct sales force by providing a digital account, created growth of 6% to 8% in sales of consultants and resellers.

Industries

Industries focused on the consumer market are also creating their own digital accounts, both for their employees and for their businesses that are partners in the distribution and resale of their products – especially if they are micro and small companies.

Thus, business establishments have card terminals, and credit and debit cards, among other services, integrating these operations into an already-existing partnership.

For example, AMBEV created a digital account for the company Donuswithout fees or a yearly enrollment fee, which allows transfers to be made via QR Code, and cash deposits, as some of the services it offers.

Logistics chains

Organizations that work with logistics chains and need to provide drivers (outsourced or their own employees) with funds for expenses such as fuel, tolls, and food, among other items, find it easy to concentrate these transactions in a digital account.

Thus, expenses with multiple suppliers are reduced (meal vouchers, fuel vouchers, etc.), and expense control and projections are facilitated.

Embedded Finance: can offering a digital account be good business for your company?

If the digital transformation of the financial market is already a reality, a large part of this progress is due to Embedded Finance <span style="color:#fff">now</span>, the phenomenon that turns companies into banks. This can also be called added financial services.

As we will see in more detail, through a Banking as a Serviceplatform, or simply BaaS, Embedded Finance allows companies that are not in the financial sector to offer products such as cards and digital accounts, credit, insurance, and loans, among other services.

What are the advantages for companies that decide to offer a digital account or other financial services? Here are just a few:

- Generating additional revenue streams by offering new products;

- Greater client loyalty by creating a robust ecosystem of solutions;

- Improved consumer experience due to the convenience of services and the provision of new means of payment;

- Aids in expanding the client base;

- Reduced operating costs, as you use your own financial structure;

- Access to a robust financial database that can help you understand consumer behavior better, and offer more adequate products and services.

Digital account for your company

By contributing to the financial inclusion of your target audience or partner, your company builds a more solid basis for a relationship with these individuals.

In addition, as we discussed in the previous section, providing a digital account also offers other benefits to companies, such as an expanded client base, reduced operating costs, and the generation of new revenue streams.

How can you create a digital account for your stakeholders?

Companies that want to create a digital account without diverting focus from their main business model, fintechs that wish to accelerate their development process, large institutions wanting to quickly test the concept, can do this through the Banking as a Service model.

The BaaS model developed by Dock is the perfect model for organizations that want to start offering financial services to their clients within just a few weeks and without having to worry about regulatory barriers.

Why offer a digital account with Dock

Banking as a Service is the basis of Dock’s Banking solution offered on the Dock Oneplatform. It allows any business or institution to offer financial services, purchasing plug-and-play technology, and just developing the front end with its brand.

Through our global platform and API module you can offer your clients a complete digital account, with all banking and loan transactions, including:

- Bill payments;

- Instant payments;

- Transfers;

- Invoice generation;

- Recharges and vouchers;

- Personal loans;

- Remunerated accounts;

- Full digital onboarding;

- Fraud prevention in partnership with leading global companies.

A plataforma da Dock também oferece, de forma integrada, todas as funcionalidades do Pix na conta digital, incluindo:

- Pix transferência: é a funcionalidade padrão do produto, de envio e recebimento de dinheiro 24 horas por dia, todos os dias.

- Pix QR Code e Pix Copia & Cola: para facilitar pagamentos via Pix, o usuário final pode fazer pagamentos com a leitura do QR Code ou copiar e colar o código para pagamento.

- Pix Cobrança: pode ser utilizado para pagamentos imediatos ou pagamentos futuros que podem incluir informações como juros, multas e outros acréscimos.

- Pix Devolução: mecanismo especial de devolução de transferência por parte do recebedor para casos de transferências incorretas.

- Pix Agendamento: funcionalidade de agendar o dia e a hora que a transferência deve ser realizada, descontando do saldo no momento escolhido.

We also handle the entire regulatory and treasury process, allowing your business to focus on what is most important: capturing new users and developing the financial solution. If you are looking for a trusted partner to make your digital account a reality through our banking solution, you can count on us, as we have already developed digital accounts for more than 100 clients, with more than one million active cards. Dock offers modular and white-label solutions on a Banking as a Service platform that is 100% API based.

Would you like to start your journey as a financial solutions provider? Learn more about Dock’s banking platform:

Digital Account: what you saw in this article

- The digital revolution transformed access and use of financial services all over the world, particularly in Latin America.

- Although cash was the main way of making and receiving payments for a very long time, today we see the digital account taking this leading role.

- Banks aren’t the only ones offering this digital experience. Companies from different sectors can also offer a digital account to their clients.

- Through a Banking as a Service platform, Embedded Finance makes it possible for companies not in the financial sector to offer products such as digital wallets and accounts, credit, insurance, and loans, among other services.

- The BaaS model developed by Dock is the perfect model for organizations that want to start offering financial services to their clients within just a few weeks, and without having to worry about regulatory barriers.

Related articles:

-

- Tokenization: what is it, and how does it impact financial services?

- The main types of digital payments, and how to offer financial services using them

- Bioeconomy: what does it have to do with banks and fintechs?

- Payroll Fintechs and the corporate benefits market: advantages and new opportunities

- Simplifying accounting through Embedded Finance | An interview with Contabilizei

-